- +91 9598678231

- vistainitiatives@gmail.com

.png)

.png)

Financial security means different things to different people. What does it mean to you?

Whatever financial security means to you, it begins with a plan for accumulating wealth, which can be called Financial Planning. The longer you wait, the harder it will be to find the money you’ll need to set aside to meet your goals for wealth accumulation. Most people think only of investments when they think of financial planning. Some also feel it has to do with mutual funds and insurance or maybe even stocks. Honestly neither of it is fully true. Financial planning is all about channelizing your financial resources (income and wealth) towards your financial goals.

As an individual/family, you have two sources of income: -

The trick is to maximise the second source, since for most of us, there isn’t much that we can do about the first one.

Start with the following two fundamental principles for a successful wealth accumulation program: -

Save at least 20%, preferably up to 35%, of your earnings consistently and throughout your earning years.

Develop a sound investment strategy and stick to it over the long term.

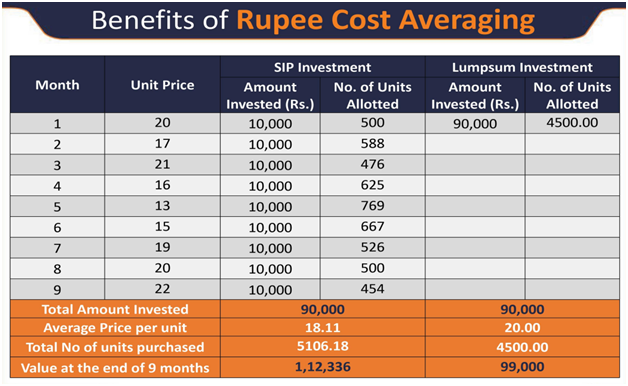

With a rupee cost averaging feature working for you, you enhance your possibility of reducing the effects of market fluctuations. Instead of trying to determine the ‘right time’ to invest, rupee cost averaging enables you to invest systematically over time. This is a commitment to invest a set amount of money, generally every month, and sticking to it regardless of market activity. While this doesn’t ensure a profit, or necessarily protect against loss in a declining market, it can help smooth out the highs and lows of volatile, market-based performance to help maintain your individual investment objectives and risk level. Because RCA involves continuous payments over a period of time, you must consider your ability to make payments in a fluctuating market.

Some people believe that the sole purpose of Financial Planners is to provide advice on investments. This is not true. Accountants, share brokers and other professionals can give you advice on some specific aspects of your financial and investment requirements. The role of a qualified Financial Planner is to look at all aspects of your lifestyle, goals and requirements and develop a financial strategy suitable for you. The recommended strategy should help you reach your goals effectively and efficiently.

At VISTA, we concentrate on the task of providing sound strategic and technical advice on an ongoing basis. The Statement of Advice includes areas like cash flow management, insurance, estate planning, risk and return assessment, strategic asset allocation, superannuation, taxation and all other issues that impact your financial strategy. The SoA is a strategic and technical guide to any financial decisions you make. Specific investment recommendations form only a part of the complete SoA. Any changes in your goals, lifestyle and circumstances should be reflected in your SoA. As professional Financial Planners we regularly review your financial strategy with you to ensure that all such changes are incorporated.

It is important to understand that there will always be risks when it comes to investing your money. The goal is to effectively manage the risk. No one can ever guarantee beyond any doubt that the value of your investments will never decrease. What a good Financial Planning organization like HumFauji Initiatives can do is put processes in place to manage the risks.

So, convinced that you need us, the special financial planning firm which has only one objective in its mind – YOUR FINANCIAL WELFARE?!

VISTA INITIATIVES established in the year 2015 with the sole aim of providing an ethical, transparent and cost-efficient platform which addresses all the financial needs of the Client.

Ananta Society, Zirakpur,

SAS Nagar Mohali

Punjab 140603

vistainitiatives@gmail.com

+91 6306194559

Copyright © Vista Initiatives. All rights reserved.

Risk Factors – Investments in Mutual Funds are subject to Market Risks. Read all scheme related documents carefully before investing. Mutual Fund Schemes do not assure or guarantee any returns. Past performances of any Mutual Fund Scheme may or may not be sustained in future. There is no guarantee that the investment objective of any suggested scheme shall be achieved. All existing and prospective investors are advised to check and evaluate the Exit loads and other cost structure (TER) applicable at the time of making the investment before finalizing on any investment decision for Mutual Funds schemes. We deal in Regular Plans only for Mutual Fund Schemes and earn a Trailing Commission on client investments. Disclosure For Commission earnings is made to clients at the time of investments.

AMFI Registered Mutual Fund Distributor – ARN-102845 | Date of initial registration – 04-Jun-2015 | Current validity of ARN – 03-Jun-2027

Important Links | Disclaimer | Disclosure | Privacy Policy | SID/SAI/KIM | Code of Conduct | SEBI Circulars | AMFI Risk Factors